What Is the Actual Impact of Tax Reform on Working Families

Federal Budget and Economy

Q.

What are the economic effects of the Revenue enhancement Cuts and Jobs Act?

A.

Most analysts expected the Tax Cuts and Jobs Act to boost economical output modestly in both the short and the longer run. So far, the testify supports the prediction for the short run. It is too soon to tell about the longer run but as notwithstanding there is lilliputian bear witness of a potent upshot on investment that could atomic number 82 to college longer-run growth.

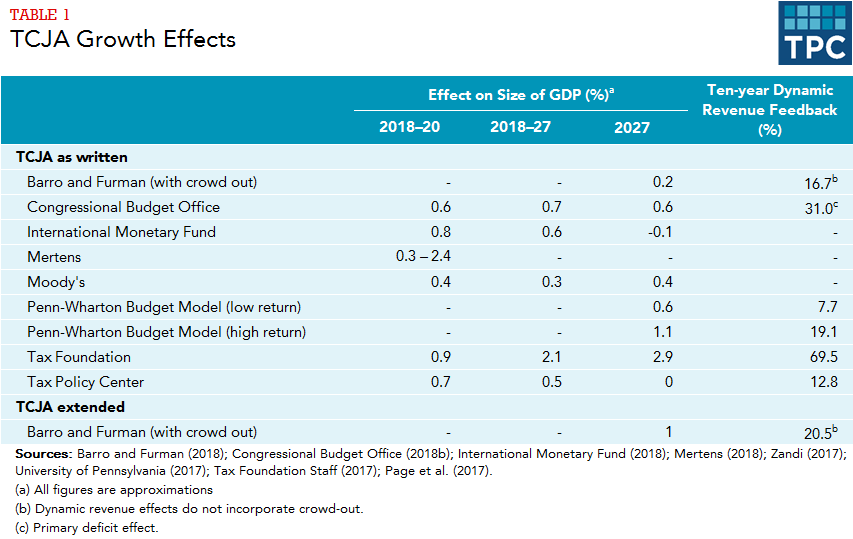

The Tax Cuts and Jobs Act (TCJA) reduced tax rates on both business and individual income, and enhanced incentives for investment past firms. Those features most likely accept raised output in the short run and volition continue to do then in the long run, but most analysts approximate the modest effects that beginning only a portion of revenue loss from the bill (table 1).

So far the TCJA has likely influenced the economy primarily by raising demand for goods and services. Cuts to private income taxes mean that most households have more afterward-tax income, which they are likely to spend. In addition, provisions such as allowing the expensing of some capital investment may take increased investment spending by firms. As businesses come across more of their goods being purchased, they reply by ramping upwardly product, boosting economical output. Growth in 2018 rose to 2.9 percent, from 2.four percent in 2017, likely due largely to the effects of TCJA on need. However, growth slowed dorsum downwardly to 2.3 percent in 2019.

Those short-run effects have likely been limited, however, for two primary reasons. Starting time, much of the tax cuts menstruation to higher-income households or to corporations, whose stock tends to be held past the wealthy. Higher-income households tend to spend less of their increases in after-tax income than lower-income households. 2nd, the revenue enhancement cut was enacted at a time when unemployment was low and output was near its potential level. Therefore, the increase in demand has been get-go by tight monetary policy, as the Federal Reserve held interest rates higher than they otherwise would have been to avoid rising inflation.

In the longer run, the TCJA is likely to affect the economic system primarily through increased incentives to work, save, and invest. Reductions in individual income tax rates mean that workers can proceed more than out of each additional dollar of wages and bacon. That will encourage people to work more hours and draw some new entrants into the labor force. However, those reduced rates are scheduled to expire at the end of 2025; after that, there is little or no tax incentive to increment work.

Lower individual taxation rates, a lower corporate tax rate, expensing of majuscule investment, and other reductions in business tax rates will increase the after-tax return to saving, encouraging households to salvage and reducing the cost of investment for firms. Those changes volition atomic number 82 to more investment, a larger capital stock, and higher output, by virtually estimates.

The increased investment must be financed by a combination of private saving, public saving (or government budget surpluses), and cyberspace lending from abroad (which could accept the form of bond purchases, portfolio investment, or directly investment of physical capital). Almost analysts, consistent with empirical enquiry, estimate that individual saving will rise only modestly in response to an increment in the after-tax rate of return. And the bill reduces public saving, by increasing the deficit. Therefore, much of any increment in investment from TCJA is likely to be financed by net strange lending. That will increase the time to come involvement and profit payments that flow to foreigners, reducing the resources available to Americans. For that reason, in examining the effects of TCJA information technology may be more illuminating to wait at changes in gross national product (which subtracts that type of payment) rather than gdp (which does not). For example, the Congressional Budget Office estimates that TCJA will boost Gdp by 0.6 percent in 2027, but—taking account of increased payments to foreigners—GNP will be up by only 0.2 pct.

It's besides shortly to gauge what TCJA's long-run affect on investment will be, but so far there is footling testify of a strong event. Investment rose in 2018, merely research by the IMF suggests that increase stemmed mostly from the short-run boost to demand. Supporting that notion, a Congressional Research Service analysis found that the types of investment that rose in 2018 were non those whose costs were reduced most past TCJA (as i would expect if the increases were driven by long-run toll factors rather than short-run demand).

Updated May 2020

Further Reading

Barro, Robert J., and Jason Furman. 2018. "Macroeconomic Effects of the 2017 Revenue enhancement Reform." Brookings Papers on Economic Activity. Washington, DC: Brookings Institution.

Congressional Budget Part. 2018. "The Upkeep and Economic Outlook: 2018–2028," Appendix B. Washington, DC: Congressional Budget Office.

Gravelle, Jane One thousand., and Donald J. Marples. 2019. "The Economic Effects of the 2017 Tax Revision: Preliminary Observations." Washington, DC: Congressional Research Service.

International Budgetary Fund. 2018. "Brighter Prospects, Optimistic Markets, Challenges Alee." World Economic Outlook Update. Washington, DC: Imf.

Articulation Committee on Tax. 2017b. "Macroeconomic Analysis of the Conference Agreement for H.R. 1, The "Tax Cuts and Jobs Act." JCX-69-17. Washington, DC: Congress of the United States.

Kopp, Emanuel, Danial Leigh, Susanna Mursula, and Suchanan Tambunlertchai. 2019. "U.S. Investment Since the Tax Cuts and Jobs Act of 2017." International monetary fund Working Paper No. 19/120. Washington, DC: International Monetary Fund.

Mertens, Karel. 2018. "The Near-Term Growth Impact of the Tax Cuts and Jobs Human activity." Research Section Working Paper 1803. Dallas: Federal Reserve Banking company.

Page, Benjamin R., Joseph Rosenberg, James R. Nunns, Jeffrey Rohaly, and Daniel Berger. 2017. "Macroeconomic Analysis of the Tax Cuts and Jobs Deed." Washington DC: Urban-Brookings Tax Policy Center.

Taxation Foundation Staff. 2017. "Preliminary Details and Analysis of the Tax Cuts and Jobs Act." Special Report No. 241. Washington, DC: Revenue enhancement Foundation.

University of Pennsylvania. 2017. "The Tax Cuts and Jobs Act, as Reported by the Conference Commission (12/15/17): Static and Dynamic Effects on the Budget and the Economy." Penn Wharton Budget Model. Philadelphia: University of Pennsylvania.

Zandi, Mark. 2017. "US Macro Outlook: A Program That Doesn't Go It Done." Moody'southward Analytics (blog), December 18.

Source: https://www.taxpolicycenter.org/briefing-book/what-are-economic-effects-tax-cuts-and-jobs-act

0 Response to "What Is the Actual Impact of Tax Reform on Working Families"

Post a Comment